Seasonal Decomposition of a Time Series (STL)

Seasonal Decomposition of a Time Series (STL) is a statistical technique used to separate out the trend, seasonality, and noise components of a given time-series data set. Seasonal Decomposition of a Time Series (STL) is an important component of data analytics and understanding temporal patterns in data.

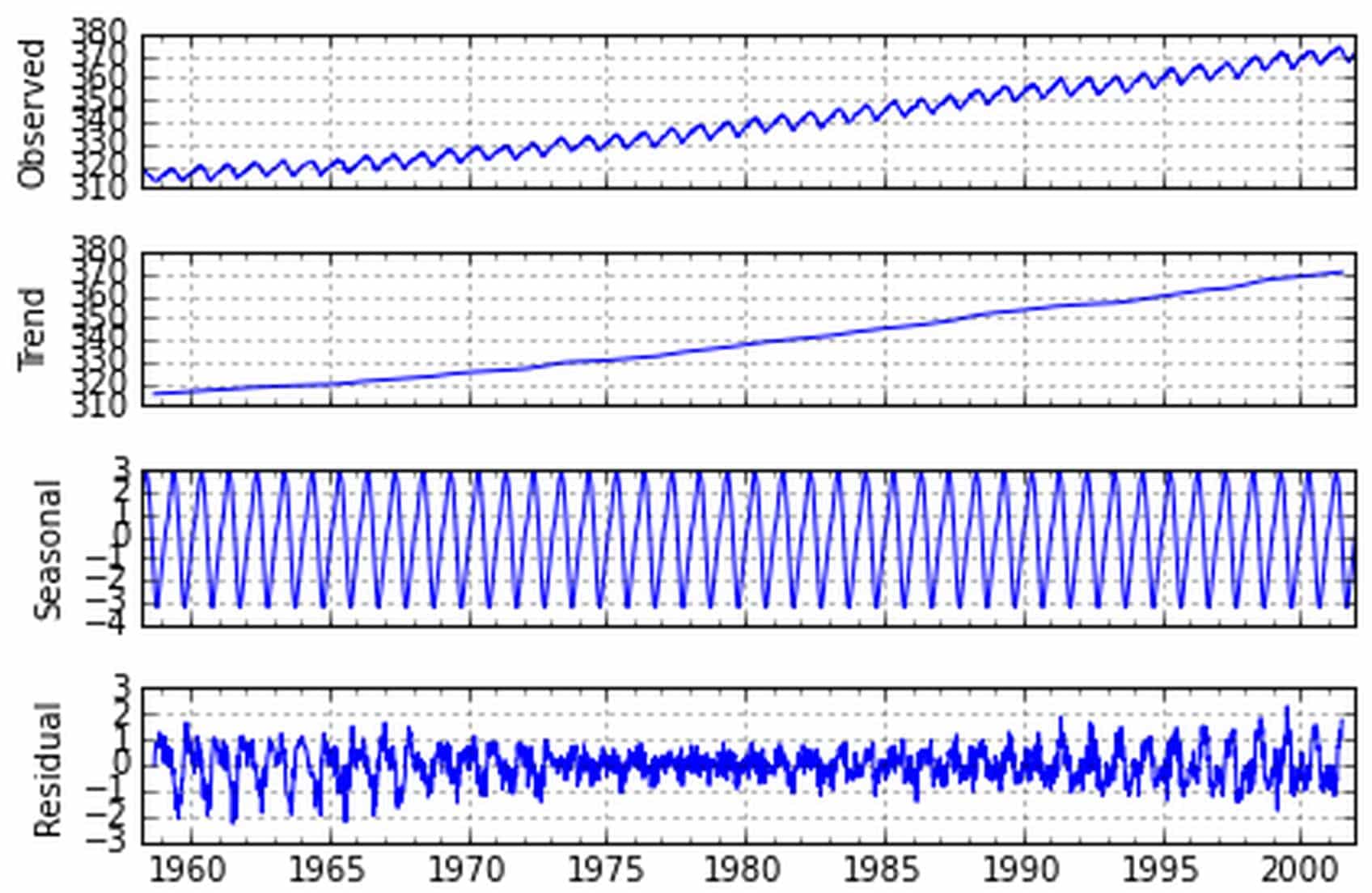

The technique itself is based on an implementation of Loess smoothing, which is used to smoothen the data. A Loess smoothing factor is applied to a given time-series data set to produce an underlying trend. The seasonal component is then derived from the subtraction of the trend from the original series. This component reflects the up-and-down fluctuations in the data that are not explained by the trend. Finally, the noise component is calculated from the residual of the two previous.

Seasonal Decomposition of a Time Series (STL) can be used in various fields, including economics, finance, and climate science. For example, it can be used to identify seasonal changes in consumer purchases. It can also be used to analyze climate fluctuations, such as the El Niño Southern Oscillation, which are closely related to seasonal weather events.

Overall, Seasonal Decomposition of a Time Series (STL) provides powerful insights into temporal patterns in data as it allows for the extraction of trend, seasonality, and noise components. It is a useful technique for understanding data in various fields, from economics to climate science.